Temporary loan repayment deferrals due to COVID-19, August 2020

Many authorised deposit-taking institutions (ADIs) have granted temporary relief to borrowers impacted by COVID-19, allowing them to defer loan repayments for a period of time. To provide greater transparency of loan repayment deferrals, APRA is publishing:

- the aggregated data obtained from all ADIs in Australia, excluding foreign branches; and

- data from ADIs with loans subject to repayment deferral.

Aggregate industry data on loans subject to repayment deferral

*the number of facilities does not necessarily indicate the number of borrowers as individual facilities with more than one repayment type may be reported more than once.

**to give an indicator of potential elevated risk in loans subject to deferral this chart compares loans subject to deferral to total loans across three key cohorts – loan to value ratio of greater than 90 per cent, investor loans and interest only loans.

An accessible version of this dashboard is available here.

Additional commentary

| Deferred loans | Total loans | Deferred loans, share of total loans |

Total | $229 billion | $2.7 trillion | 8.5% |

Housing | $160 billion | $1.8 trillion | 9.0% |

SME | $53 billion | $325 billion | 16.2% |

As at 31 August, data submitted by all ADIs indicates that $229 billion worth of loans have been granted temporary repayment deferrals, which is around 8.5 per cent of total loans outstanding. Housing loans make up the majority of total loans granted repayment deferrals, although small business loans have a higher incidence of repayment deferral with 16.2 per cent of small business loans subject to repayment deferral, compared with 9.0 per cent of housing loans.

Exits from deferral continue to outweigh new entries for the second straight month in August, with $24 billion loans expiring or exiting deferral and $14 billion of entries approved or extended. The pace of exits slowed over the month, with total exits decreasing 41 per cent from $40 billion in July. The majority of these loans have returned to a performing status.

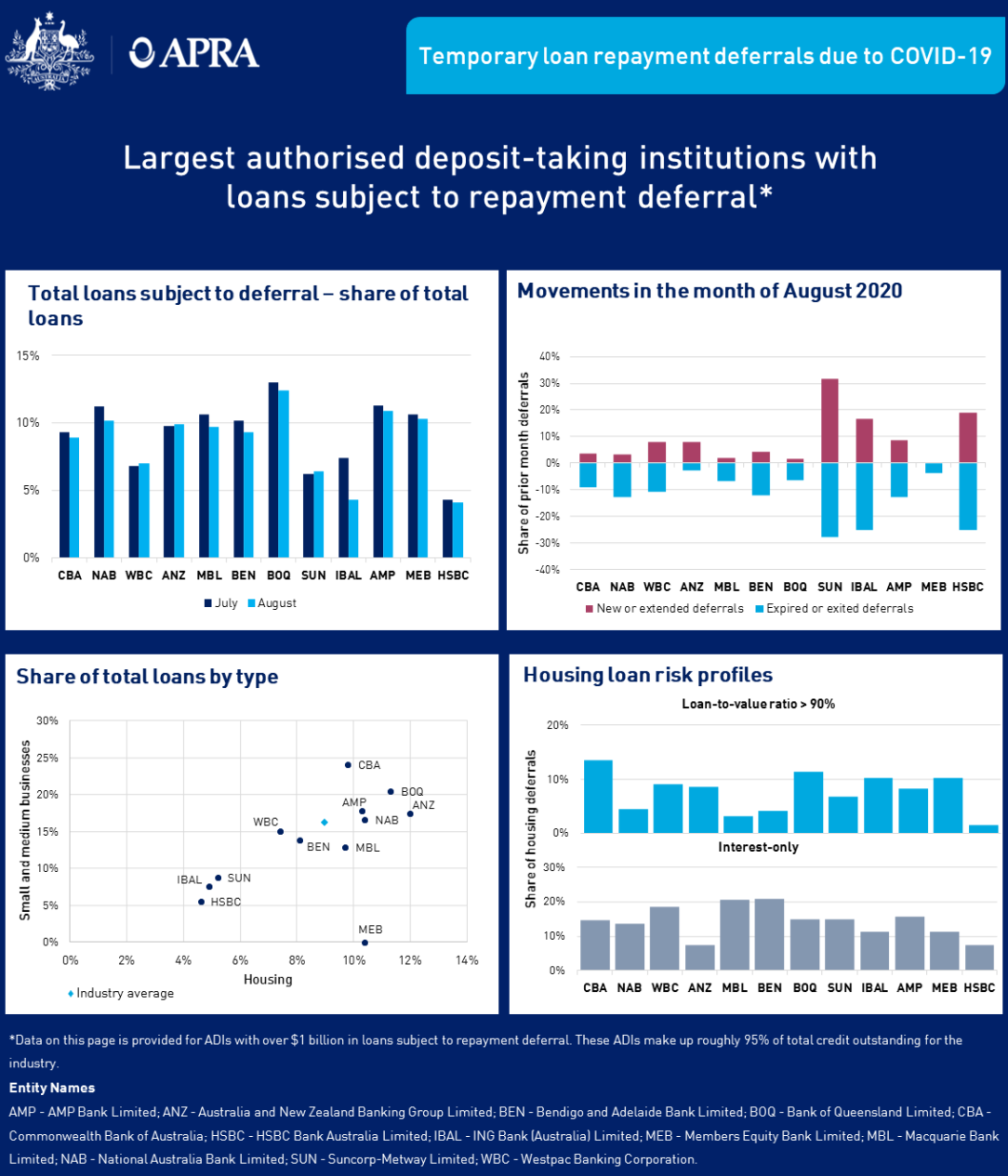

Largest ADIs with loans subject to repayment deferral

An accessible version of the dashboard is available here.

Explanatory notes

This data is sourced from the domestic loan portfolios1 of APRA-regulated authorised deposit-taking institutions (ADIs), excluding foreign branches. The spreadsheet below contains data for all ADIs with total loans subject to temporary repayment deferral of greater than $20 million and more than 20 deferred facilities in any given reporting period. In addition, for privacy reasons, fields are masked where there is a non-zero value below $10 million or there are less than 20 facilities. For an entity where either the "new or extended in the month" field or the "expired or exited in the month" field falls below this threshold, both of these fields are masked.

Changes in total loans subject temporary repayment deferral occur due to several factors. These factors include (but are not limited to) new deferrals, exits from deferral, addition of interest charges on existing deferrals and customers paying down their loans subject to deferral. Note that the graphs displaying “movements” (top right on both dashboards above) only include exits, new or extended deferrals but do not include other factors that change the value of total loans subject to temporary repayment deferral. Also note that, when a borrower’s loan repayment deferral is extended it is reported in this data as both "expired or exited in the month" (as the initial deferral has expired) and "new or extended in the month" (as it has been extended).

All data has been submitted to APRA on a best endeavours basis under relatively tight timeframes. As a result, data may be revised in future reports.

APRA will continue to publish this information on a monthly basis until loans subject to repayment deferrals are no longer a notable component of the ADI industry’s total loan portfolio.

Footnote:

1Domestic loan portfolio refers to loans provided within Australia on the balance sheet of the licenced ADI.

Glossary

ADI refers to an authorised deposit-taking institution, meaning a body corporate authorised under section 9 of the Banking Act 1959, to carry on banking business in Australia (e.g. a bank, building society or credit union).

Expiring or exiting repayment deferral refers to the credit outstanding of loans that were no longer subject to repayment deferral or were extended beyond their original deferral terms.

Facility refers to one or more accounts/lending agreements that are for the same borrower(s), and are approved at the same point in time and/or as part of the same application for the same purpose class (and property purpose if housing), and differ only by characteristics relating to interest rate type (fixed interest rate or variable interest rate) and/or repayment type (interest-only or amortising). The number of facilities does not necessarily indicate the number of borrowers as individual facilities with more than one repayment type may be reported more than once.

Housing loans are loans to resident households for the purpose of housing.

Interest-only loans are loans on which only interest is paid during a set period and no principal is automatically amortised. These loans will typically revert to principal-and-interest repayments at the end of the interest-only period.

Investment loans are loans for the purpose of housing, where the funds are used for a residential property that is not owner-occupied. This refers to the occupation status of the residential property that has been obtained, not the occupation status of the property used as security. It includes holiday or vacation homes and part-time residences that are not the borrower’s principal place of residence.

Loan-to-value ratio (LVR) is the ratio of the outstanding amount of the loan to the value of the property that secures the exposure.

Loans refers to loans and finance leases gross of provisions. Loans are financial assets that are created when a creditor lends funds directly to a debtor, and is evidenced by non-negotiable documents. Finance leases are leases that transfer substantially all the risks and rewards incidental to the ownership of an asset.

Loans subject to repayment deferral refers to the credit outstanding of loans where ADIs have granted temporary relief to borrowers impacted by the economic effects of COVID-19, allowing them to defer loan repayments for a set period of time.

New or extended loan deferrals refers to the credit outstanding of repayment deferrals that have been approved or extended.

Small and medium business (SME) loans refers to loans to small and medium enterprises with less than $10 million in total debt facilities outstanding.

For more information

Email dataanalytics@apra.gov.au or mail to

Manager, External Data Reporting

Australian Prudential Regulation Authority

GPO Box 9836, Sydney NSW 2001Looking for discontinued publications?

Search historical snapshots of APRA's website on the Australian Government web archive.